Navigating the world of business expenses can be tricky. Are you maximizing your deductions or leaving money on the table? Did you know that many businesses miss out on valuable deductions simply because they aren't aware of the rules? Luckily, IRS Publication 463 is here to help, but let’s be honest – IRS documents aren’t exactly known for being light reading.

That’s where this guide comes in. We'll break down IRS Publication 463 in an easy-to-consume format, so you can confidently handle your business expenses.

What is IRS Publication 463?

IRS Publication 463 is a comprehensive guide that explains what business-related expenses are deductible. It covers the ins and outs of deducting expenses for:

- Travel

- Non-entertainment-related meals

- Gifts

- Transportation

It also provides guidance on record-keeping requirements and how to report these expenses on your tax return.

Why is IRS Publication 463 Important for Business Owners?

Understanding IRS Publication 463 is crucial for business owners because it can directly impact your bottom line. By knowing what expenses are deductible and how to properly claim them, you can:

- Reduce your taxable income

- Lower your tax liability

- Maximize your tax savings

Essentially, it's about keeping more of your hard-earned money.

Breaking Down IRS Publication 463

The IRS Publication 463 is divided into six chapters. In this section, we’ll dive into its specifics in great detail, breaking down even the trickiest concepts. Think of this as getting a plain English translation, so anyone, even if you're brand new to this, can understand and make the most of the IRS's guidance.

Chapter 1: Travel

Chapter 1 of IRS Publication 463 focuses on travel expenses, which are defined as ordinary and necessary expenses while traveling away from your tax home for business, profession, or job.

Traveling Away From Home

To deduct travel expenses, you must be considered "away from home." This means your duties require you to be away from the general area of your tax home substantially longer than an ordinary day's work, and you need to sleep or rest to meet the demands of your work while away from home.

- Tax Home: Your tax home is generally your regular place of business or post of duty, regardless of where you maintain your family home. If you have more than one regular place of business, your main place of business is your tax home.

- Tax Home vs. Family Home: You cannot deduct the cost of traveling between your tax home and your family home, nor can you deduct meals and lodging while at your tax home.

- Temporary Assignment: If your assignment away from your main place of work is temporary (generally expected to last for one year or less), your tax home doesn’t change, and you can deduct travel expenses.

To make this even easier: Let’s say your main office is in Austin, but you have a temporary work assignment in Dallas. In this case, you can deduct travel expenses between Austin and Dallas. However, if your assignment in Dallas is expected to last more than a year, Dallas becomes your new tax home, and you can no longer deduct those expenses.

What Travel Expenses Are Deductible?

Ordinary and necessary expenses you have when you travel away from home on business can be deductible.

Tax Deductible Travel Expenses Include

- Transportation costs (airfare, train, etc.)

- Taxi, commuter bus, and airport limousine fares

- Baggage and shipping costs

- Car operating expenses (actual expenses or standard mileage rate)

- Lodging and non-entertainment-related meals

- Cleaning (dry cleaning and laundry)

- Telephone (business calls)

- Tips

- Other similar ordinary and necessary expenses

To make this even easier: Imagine you’re on a business trip. You can deduct the cost of your flight, the taxi to your hotel, the hotel itself, and even the cost of dry cleaning your business attire.

Meals

When traveling away from home on business, you can deduct a portion of the cost of meals.

- 50% Limit: Generally, you can only deduct 50% of your unreimbursed meal expenses.

- Actual Cost vs. Standard Meal Allowance: You can use the actual cost of your meals or the standard meal allowance to figure out your deductible expense. The standard meal allowance is a set amount for daily meals and incidental expenses (M&IE), which varies depending on where and when you travel.

To make this even easier: You can deduct 50% of your meal expenses, but they can’t be lavish or extravagant. You can either track the actual cost of each meal or use a standard meal allowance. For example, instead of keeping every single receipt, you could use the standard meal allowance, which simplifies record-keeping.

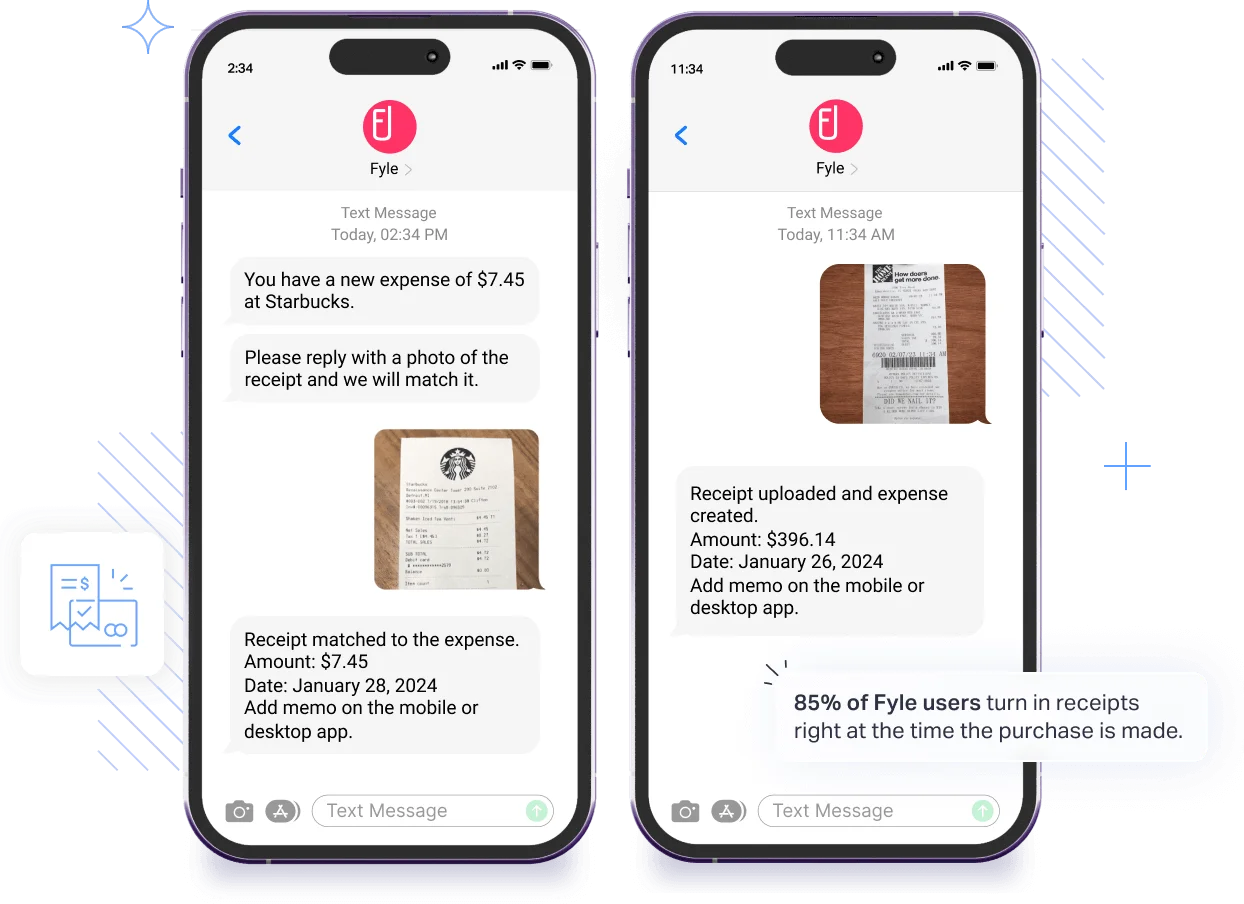

How Sage Expense Management (formerly Fyle) Can Help

Sage Expense Management lets you track and submit receipts from everyday apps like text messages, Slack, Gmail, or Outlook. It automatically creates, codes, and submits an expense report while automatically checking for compliance.

Travel in the United States

The deduction of travel expenses within the United States depends on whether the trip was primarily for business or personal reasons.

- Trip Primarily for Business: You can deduct all your travel expenses. If you extend your stay for a vacation or personal activities, you can only deduct your business-related travel expenses.

- Trip Primarily for Personal Reasons: The entire cost of the trip is a non-deductible personal expense. However, you can deduct expenses you have at your destination that are directly related to your business.

To make this even easier: If you take a trip mainly for business and add a few personal days, you can deduct the business portion of your travel expenses. But, if the trip is mainly for vacation, you can only deduct expenses directly related to business activities.

Travel Outside the United States

If any part of your business travel is outside the United States, your deductions for the cost of getting to and from your destination may be limited.

- Travel Entirely for Business: You can deduct all your travel expenses.

- Travel Considered Entirely for Business: Even if you didn’t spend your entire time on business activities, your trip can be considered entirely for business under certain exceptions, such as not having substantial control over arranging the trip, being outside the United States for a week or less, spending less than 25% of the total time outside the U.S. on non-business activities, or establishing that a personal vacation wasn’t a major consideration.

- Travel Primarily for Business: If your trip outside the United States was primarily for business, but you spend some of your time on other activities, you can only deduct the business portion of your costs.

To make this even easier: If you travel to Canada for a conference and spend the weekend sightseeing, you can deduct the cost of traveling to and from the conference, but not the expenses for your sightseeing days.

Luxury Water Travel

If you travel by ocean liner, cruise ship, or other form of luxury water transportation for business purposes, there are limits on the amount you can deduct.

- Daily Limit: The limit is twice the highest federal per diem rate allowable at the time of your travel.

- Meals and Entertainment: If these expenses are separately stated, they are subject to the 50% limit before applying the daily limit.

To make this even easier: If you take a cruise for a business conference, your deduction for the cruise fare is limited.

Conventions

You can deduct your travel expenses when you attend a convention if you can show that your attendance benefits your trade or business.

- Conventions Held Outside the North American Area: You can’t deduct expenses unless the meeting is directly related to the active conduct of your trade or business, and it is as reasonable to hold the meeting outside the North American area as within it. The North American area includes locations like Canada, Mexico, and certain Caribbean countries.

- Cruise Ships: You can deduct up to $2,000 per year of expenses for attending conventions, seminars, or similar meetings held on cruise ships, under specific conditions.

To make this even easier: If you attend a business convention in the United States, you can deduct your travel expenses. If the convention is held overseas, there are stricter rules for deducting those expenses.

Chapter 2: Meals and Entertainment

Chapter 2 of IRS Publication 463 covers the rules for deducting expenses for meals and entertainment.

Entertainment

The deduction of entertainment expenses is generally no longer allowed.

- Entertainment Defined: Entertainment includes any activity generally considered to provide entertainment, amusement, or recreation, such as entertaining guests at nightclubs, social, athletic, and sporting clubs, theaters, sporting events, on yachts, or on hunting, fishing, vacation, and similar trips.

- Exceptions to the Rules: There are a few exceptions to the general rule of non-deductibility, including entertainment treated as compensation, recreational expenses for employees (like a holiday party), expenses related to attending business meetings of certain exempt organizations, and entertainment sold to customers (such as a floor show by a nightclub).

- Examples of Nondeductible Entertainment: This includes entertainment events, entertainment facilities, and club dues.

To make this even easier: You can no longer deduct the cost of taking a client to a sporting event or a concert. Club dues for country clubs and airline clubs are also not deductible. However, if you provide a holiday party for your employees, that expense is generally deductible.

Meals

You can deduct 50% of the cost of business meals if you (or an employee) are present and the food or beverages aren’t considered lavish or extravagant.

- 50% Limit: In general, you can deduct only 50% of your business-related meal expenses unless an exception applies.

- Exceptions to the 50% Limit: There are several exceptions, including expenses treated as compensation, employee’s reimbursed expenses, self-employed reimbursed expenses, recreational expenses for employees, advertising expenses, and sale of meals.

- Individuals Subject to “Hours of Service” Limits: You can deduct a higher percentage (80%) of your meal expenses while traveling away from your tax home if the meals take place during any period subject to the Department of Transportation’s “hours of service” limits.

To make this even easier: You can generally deduct 50% of the cost of taking a client out for a business meal as long as it's not lavish or extravagant. However, if your employer reimburses you for the meal under an accountable plan, you are not subject to this 50% limit.

Chapter 3: Gifts

Chapter 3 of IRS Publication 463 covers the rules and limitations for deducting business gifts.

Gifts

- $25 Limit: You can deduct no more than $25 for business gifts you give directly or indirectly to each person during your tax year.

- Incidental Costs: Incidental costs, such as engraving or packaging, are generally not included in the $25 limit, as long as they don’t add substantial value to the gift.

- Exceptions: Items that cost $4 or less with your name clearly and permanently imprinted and are widely distributed, and signs, display racks, or other promotional material to be used on the business premises of the recipient are not considered gifts for purposes of the $25 limit.

To make this even easier: If you give a client a holiday gift basket, you can deduct up to $25 of the cost. The cost of the basket itself is included in the $25 limit if it has substantial value.

Chapter 4: Transportation

Chapter 4 of IRS Publication 463 discusses expenses you can deduct for business transportation when you aren’t traveling away from home.

Transportation Expenses

Transportation expenses include the ordinary and necessary costs of:

- Getting from one workplace to another within your tax home.

- Visiting clients or customers.

- Going to a business meeting away from your regular workplace.

- Getting from your home to a temporary workplace when you have one or more regular places of work.

Transportation expenses do not include

- Expenses you have while traveling away from home overnight (those are travel expenses).

- Daily transportation expenses you incur while traveling from home to one or more regular places of business (those are generally non-deductible commuting expenses).

To make this even easier: If you travel between client meetings during the workday, those transportation costs are deductible. However, the costs of your regular commute to and from your office are not deductible.

Car Expenses

If you use your car for business purposes, you can deduct car expenses.

Methods for Deducting Car Expenses

You can generally use one of two methods:

- Standard Mileage Rate: For 2026, this rate is $0.725 per mile for business use. If you use this rate, you cannot deduct actual car expenses like depreciation, lease payments, or gasoline.

- Actual Car Expenses: If you choose this method, you can deduct actual costs like depreciation, lease payments, registration fees, insurance, repairs, gas, and tolls.

Also Read

Business and Personal Use

If you use your car for both, you must divide your expenses accordingly. For example, if you drive 20,000 miles a year and 12,000 are for business, you can only deduct 60% of the car's operating costs.

Also Read

Depreciation

If you use actual expenses, you can deduct depreciation, which is recovering the cost of your car over time. There are limits to depreciation deductions.

Section 179 Deduction

You can elect to deduct all or part of the cost of a car that qualifies as property up to a limit in the year you place the property in service.

Leasing a Car

If you lease a car, you can deduct the portion of the lease payment that is for business use. If you lease a car for 30 days or more, you may have to reduce your lease payment deduction by an "inclusion amount."

How Sage Expense Management (formerly Fyle) Can Help

Using Google Maps, Sage Expense Management accurately tracks mileage from start to destination, automatically applying rates. Employees can set recurring trips, add travel purposes, and manage bulk mileage. For precise tracking, commute distances are automatically deducted, streamlining the entire process.

Chapter 5: Recordkeeping

Chapter 5 of IRS Publication 463 emphasizes the importance of keeping accurate records for your business expenses.

How to Prove Expenses

If you deduct travel, gift, or transportation expenses, you must be able to prove (substantiate) certain elements of those expenses.

Adequate Records

You should keep records in an account book, diary, log, or similar record. You also need documentary evidence, like receipts, canceled checks, or bills, to support your expenses.

Documentary Evidence Exception

Documentary evidence is not needed for:

- Expenses while traveling away from home accounted for under an accountable plan using a per diem allowance method.

- Expenses (other than lodging) less than $75.

- Transportation expenses where a receipt isn’t readily available.

What is Adequate Evidence?

Documentary evidence is adequate if it shows the amount, date, place, and essential character of the expense. For example, a hotel receipt should include the name and location of the hotel, the dates you stayed, and separate amounts for charges like lodging, meals, and phone calls.

A restaurant receipt should include the name and location of the restaurant, the number of people served, and the date and amount of the expense.

Also Read

Canceled Check

A canceled check with a bill from the payee can prove the cost, but a canceled check alone is not sufficient to prove a business expense.

Timely Kept Records

You should record expenses at or near the time of the expense or use. A weekly log is considered a timely kept record.

Proving Business Purpose

You generally need a written statement of the business purpose of an expense, but the degree of proof varies.

To make this even easier: Imagine you’re taking a client out for dinner. A receipt with the restaurant's name, the date, the number of people, and the total cost is enough to prove the expense. But remember, you also might need to jot down the business purpose of the dinner to have a solid record.

What if I Have Incomplete Records?

If you don’t have complete records, you must prove the expense with your written or oral statement containing specific information about the expense, as well as other supporting evidence.

- Supporting Evidence: If the element is the description of a gift or the cost, time, place, or date of an expense, the supporting evidence must be direct or documentary evidence. If the element is the business relationship of your guests or the business purpose of the amount spent, the supporting evidence can be circumstantial.

- Sampling: You can keep records for part of the tax year and use that record to prove the amount of business or investment use for the entire year, if you can demonstrate that the periods are representative of the use throughout the tax year.

- Exceptional Circumstances: If you couldn’t get a receipt due to the nature of the situation, you can still satisfy the requirements with other evidence, if you meet certain conditions.

- Destroyed Records: If you can’t produce a receipt due to reasons beyond your control, you can prove a deduction by reconstructing your records or expenses.

To make this even easier: Let’s say you lost a receipt. You can still prove the expense with a statement explaining the expense and other evidence, like a credit card statement showing the charge.

How Sage Expense Management (formerly Fyle) Can Help

Sage Expense Management's digital record-keeping eliminates the risk of lost receipts. In fact, 85% of our customers submit receipts right at the time of purchase using just a text message!

Separating and Combining Expenses

- Separating Expenses: Each separate payment is generally considered a separate expense.

- Combining Items: You can make one daily entry in your record for reasonable categories of expenses, such as taxi fares, telephone calls, or other incidental travel costs. Expenses of a similar nature during a single event are considered a single expense.

To make this even easier: If you take a client to dinner and then to a show, the dinner and show tickets are separate expenses. However, you can combine your taxi fares for the day into a single entry.

How Long to Keep Records and Receipts

You must keep records as long as they may be needed for the administration of any provision of the Internal Revenue Code, generally 3 years from the date you file the income tax return on which the deduction is claimed.

- Reimbursed Expenses: Employees who give records to their employers and are reimbursed generally don’t have to keep copies, unless they claim deductions exceeding reimbursements, are reimbursed under a nonaccountable plan, their employer doesn’t use adequate accounting procedures, or they are related to their employer.

To make this even easier: Keep your expense records for at least 3 years after filing your tax return. If your employer reimburses you for expenses, you might not need to keep those records, but there are exceptions.

Examples of Records

IRS Publication 463 provides examples of record-keeping formats, such as a daily business mileage and expense log and a weekly traveling expense record.

Chapter 6: How to Report

Chapter 6 of IRS Publication 463 explains how and where to report the expenses discussed in the publication.

Where to Report

- Self-Employed: Report income and expenses on Schedule C (Form 1040) or Schedule F (Form 1040) (for farmers).

- Both Self-Employed and an Employee: Keep separate records for each activity and report them accordingly.

- Employees: Generally, complete Form 2106 to deduct employee business expenses.

- Employer-Provided Vehicle: If your employer provides a vehicle, you may be able to deduct actual operating expenses, but you can’t use the standard mileage rate.

To make this even easier: Where you report your expenses depends on whether you are self-employed or an employee. Self-employed individuals use Schedule C or F, while employees generally use Form 2106.

Reimbursements

How you report expenses and reimbursements depends on whether your employer uses an accountable plan or a nonaccountable plan.

Accountable Plans

To be an accountable plan, your employer’s reimbursement arrangement must meet certain rules, including having a business connection, requiring you to adequately account for expenses, and requiring you to return any excess reimbursement or allowance within a reasonable period.

Per Diem and Car Allowances

If your employer reimburses you using a per diem or car allowance, it can satisfy the adequate accounting requirements under certain conditions, such as the allowance being similar in form and not more than the federal rate and you proving the time, place, and business purpose of your expenses to your employer.

The federal rate can be figured using methods like the regular federal per diem rate, the standard meal allowance, the high-low rate, the standard mileage rate, or a fixed and variable rate (FAVR).

Nonaccountable Plans

A nonaccountable plan is a reimbursement arrangement that doesn’t meet the rules for accountable plans.

Also Read

To make this even easier: If your employer reimburses you for expenses, it will either be through an accountable plan or a nonaccountable plan. Accountable plans have specific rules, like requiring you to provide proof of your expenses. Nonaccountable plans are less strict, but the reimbursements are included in your taxable wages.

How Sage Expense Management Can Help

Simplify your reimbursement process with Sage Expense Management. Not only can you effortlessly track and categorize reimbursements, ensuring clarity on accountable and nonaccountable plans for tax purposes, but you can also repay employees directly via ACH (US only).

Streamline payouts to multiple employees with a single click, and leverage Sage Expense Management's insightful reports to simplify tax preparation."

Rules for Independent Contractors and Clients

This section provides rules for independent contractors who incur expenses on behalf of a client or customer.

- Accounting to Your Client: If you receive a reimbursement or allowance for expenses you incurred on behalf of a client, you should provide an adequate accounting of these expenses to your client.

- Required Records for Clients or Customers: Clients or customers generally don’t have to keep records to prove reimbursements or allowances given to independent contractors, unless they reimburse the contractor for entertainment expenses and the contractor adequately accounts for these expenses.

To make this even easier: If you are an independent contractor, you need to provide your client with a record of the expenses you incurred on their behalf. If you are the client, you generally don’t need to keep those records unless they include entertainment expenses.

How to Use Per Diem Rate Tables

This section provides information about per diem rate substantiation methods and transition rules.

- Two Substantiation Methods: The high-low method and the regular federal per diem rate method are discussed.

- Transition Rules: This section explains the transition period, which covers the last 3 months of the calendar year, and the choices you have regarding using the new rates or continuing with the old rates.

Also Read

To make this even easier: The IRS provides methods to simplify how you prove your travel expenses using per diem rates. These rates change, and there are rules for how to handle those changes at the end of the year.

Completing Form 2106

This section provides a brief description of how employees complete Form 2106.

- Car Expenses: If you used a car for your job, you may be able to deduct certain car expenses, which are generally figured on Form 2106, Part II.

- Reimbursements: If you were reimbursed under an accountable plan and want to deduct excess expenses that weren’t reimbursed, you may have to allocate your reimbursement.

- Limits on Employee Business Expenses: Employee business expenses may be subject to limits, such as the limit on meals and entertainment, and the limit on total itemized deductions.

To make this even easier

Form 2106 is used to report employee business expenses. The way you complete it depends on factors like whether you are claiming car expenses or how you were reimbursed.

Special Rules

This section discusses special rules that apply to Armed Forces reservists, government officials who are paid on a fee basis, performing artists, and disabled employees with impairment-related work expenses.

- Armed Forces Reservists: If you are a member of a reserve component of the Armed Forces and travel more than 100 miles from home in connection with your services as a reservist, you can deduct your travel expenses as an adjustment to gross income.

- Officials Paid on a Fee Basis: Certain fee-basis officials can claim their employee business expenses on Form 2106.

- Expenses of Certain Performing Artists: Performing artists may qualify to deduct their employee business expenses as an adjustment to gross income if they meet certain requirements, such as having performing arts-related business expenses that are more than 10% of their gross income from the performance of those services and meeting certain income thresholds.

- Impairment-Related Work Expenses of Disabled Employees: If you are an employee with a physical or mental disability, your impairment-related work expenses aren’t subject to the 2%-of-adjusted-gross-income limit.

To make this even easier: Certain groups of taxpayers have specific rules for deducting business expenses. For example, performing artists can deduct expenses as an adjustment to gross income if they meet certain criteria.

How to Get Tax Help

IRS Publication 463 provides information on various resources for tax help.

Free Options for Tax Preparation

The IRS offers various free options, including:

- Direct File: A free way to file individual federal tax returns online directly and securely with the IRS.

- Free File: Prepare and file your federal individual income tax return for free using software or Free File Fillable Forms..

- VITA (Volunteer Income Tax Assistance): Free tax help to people with low-to-moderate incomes, persons with disabilities, and limited-English-speaking taxpayers.

- TCE (Tax Counseling for the Elderly): Free tax help for all taxpayers, particularly those 60 years of age and older.

- MilTax: Free tax services offered by the Department of Defense through Military OneSource for members of the U.S. Armed Forces and qualified veterans.

How Sage Expense Management Can Help

Sage Expense Management is designed to simplify and streamline expense management for businesses of all sizes. Here’s how it aligns with IRS Publication 463 and makes compliance easier:

- Real-time Credit Card Feeds: Sage Expense Managements directly integrates with all major credit card networks to give you real-time text notifications for all business credit card transactions. You can reply to this with a picture of the receipt for instant reconciliation. This is especially helpful for travel expenses, as it provides a clear record of when and where expenses were incurred, supporting the requirements outlined in Publication 463.

- Automated Receipt Capture: Employees can easily submit receipts via SMS, email, or the mobile app, creating a centralized and organized record of all transactions. This feature directly addresses the record-keeping requirements of Publication 463, ensuring you have the necessary documentary evidence for your expenses.

- Policy Enforcement: Sage Expense Management helps businesses enforce spending policies and prevent non-compliant expenses, reducing the risk of errors.

- Instant AI Spend Insights: Sage Expense Management's CoPilot offers an immediate, AI-driven view of all employee credit card expenses. Finance teams can analyze transactions by categories, merchants,and projects, using simple conversational queries.

- Project Spend Tracking: It enables admins to allocate spend to different dimensions like Projects, Cost Codes, Locations, and Departments.